The Great Recession Revisited.

Recently, a facebook friend posted an old Forbes article from 2009, blaming the entire financial crisis on the Federal Government. I wrote a couple of previous posts here and here rebutting that idea, but I thought it would be interesting to look at it in relation to the specific Forbes article in question. Lets take a look at the details.

The Forbes article states at the very beginning:

“the collapse of the bubble would not have led to a worldwide recession and credit crisis if almost 40% of all U.S. mortgages–25 million loans–were not of the low quality known as subprime or Alt-A.”

False. The number was not 40%. It was about half that, at 21% for it’s highest figure. That peaked in 2004.

Next:

“These loans were made to borrowers with blemished credit, or involved low or no down payments, negative amortization and limited documentation of income.”

The first part… That has been a feature of subprime loans since… Well.. Since that financial vehicle was invented by banks in the first place. Let’s look at a bit of history about the creation of the subprime loan:

Many factors have contributed to the growth of subprime lending. Most fundamentally, it became legal. The ability to charge high rates and fees to borrowers was not possible until the Depository Institutions Deregulation and Monetary Control Act (DIDMCA) was adopted in 1980. It preempted state interest rate caps. The Alternative Mortgage transaction Parity Act (AMTPA) in 1982 permitted the use of variable interest rates and balloon payments. These laws opened the door for the development of a subprime market, but subprime lending would not become a viable large-scale lending alternative until the Tax Reform Act of 1986 (TRA). The TRA increased the demand for mortgage debt because it prohibited the deduction of interest on consumer loans, yet allowed interest deductions on mortgages for a primary residence as well as one additional home.

Note that the development of the subprime mortgage was encouraged by the Community Reinvestment Act, signed into law in 1977.

“The loans’ unprecedentedly high rates of default are what is driving down housing prices and weakening the financial system.”

And on that, Forbes notes:

“On a parallel track was the Community Reinvestment Act. New CRA regulations in 1995 required banks to demonstrate that they were making mortgage loans to under-served communities, which inevitably included borrowers whose credit standing did not qualify them for a conventional mortgage loan.”

The author of the article in question note:

“In 1992, Congress gave a new affordable housing “mission” to Fannie and Freddie, and authorized the Department of Housing and Urban Development to define its scope through regulations….

Shortly thereafter, Fannie Mae, under Chairman Jim Johnson, made its first “trillion-dollar commitment” to increase financing for affordable housing. What this meant for the quality of the mortgages that Fannie–and later Freddie–would buy has not become clear until now.”

OK. But how much did subprime mortages grow in this period?

It did experience growth in this peroid, but it didn’t take off. It only started it’s astronomical rise in and after 2003. What caused this suddden rise? Again, to Forbes:

“Shortly after these new mandates went into effect, the nation’s homeownership rate–which had remained at about 64% since 1982–began to rise, increasing 3.3% from 64.2% in 1994 to 67.5% in 2000 under President Clinton, and an additional 1.7% during the Bush administration, before declining in 2007 to 67.8%.”

Forbes then says:

There is no reasonable explanation for this sudden spurt, other than a major change in the standards for granting a mortgage or a large increase in the amount of low-cost funding available for mortgages. The data suggest that it was both. ”

“From 1994 to 2003, Fannie and Freddie’s purchases of mortgages, as a percentage of all mortgage originations, increased from 37% to an all-time high of 57%, effectively cornering the conventional conforming market.”

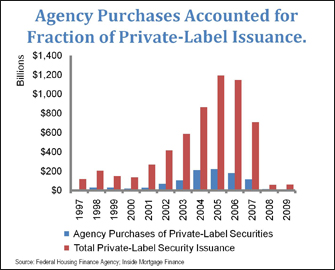

First, here is a chart showing just how badly Freddy and Fannie were eclipsed by privately issued subprime loans.

Note that the government organization only increased their purchasing of loans as the private sector grew, and never enough to meet the pace.

And there still was no financial meltdown in 2003. That didn’t come about until 2007 / 2008. What was Fannie Mae / Freddy Masc ownership like then?

Here’s a chart showing total ownership in 2006, approaching the height of the housing boom.

So nope, Forbes is wrong on this point as well.

Forbes had claimed this:

“From 1995 until 2004, subprime loans by the traditional subprime lenders like Countrywide averaged slightly more than 5% of all mortgages, far too few to account for the growth in either homeownership or the housing bubble.”

Obviously, that doesn’t jibe with the chart above.

So, why did that spike so hard after 2004? Speculation in the mortgage markets. (taken from this article)

The question here is… Why would housing loans take down the entire financial system???? There are a couple of puzzle pieces that are missing throughout the whole article… Mortagae Backed Securities (MBS’s).

Yes, the government did encourage more lending to those with lower incomes, but it was doing that for a decade before the bubble formed, and the housing market didn’t explode in either the economic downturn at the bursting of the dot-com bubble, or the economic dip that occured after the 9/11 attacks.

But, the government did not require the banks to issue loans with absolutely no credit check, or issue loans with no background check to make sure the applicant even had a job. The government did not require the banks to sell, and resell, and repackage, and resell those repackaged loans until no one had ny idea what they were buying. The government did not do this. The banks did. To blame the government is like saying it’s my dad’s fault that I robbed the bank because he threatened that if I don’t go out and earn money to pay rent, he’s going to kick me out of the house.

The reason the housing market brought the whole financial system to its knees is because the system had been way overexposed thought the over-investment in mortgage backed securities bound together by unregulated credit default swaps.

Futher, Forbes wishes to make the CRA the culprit in the mess, by saying that the CRA regulations caused the mess. Did it? Barry Ritholtz note:

“if the CRA was to blame, the housing boom would have been in CRA regions; it would have made places such as Harlem and South Philly and Compton and inner Washington the primary locales of the run up and collapse. Further, the default rates in these areas should have been worse than other regions.

What occurred was the exact opposite: The suburbs boomed and busted and went into foreclosure in much greater numbers than inner cities. The tiny suburbs and exurbs of South Florida and California and Las Vegas and Arizona were the big boomtowns, not the low-income regions. The redlined areas the CRA address missed much of the boom; places that busted had nothing to do with the CRA.”

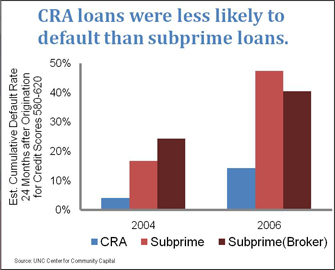

He notes that by 2006, only 28% of all mortgage originated in banks that fell under CRA jurisdiction. Also, he points out that those mortgages that were issued though CRA actually defaulted LESS than those issue outside that system, which were the types of loans that Countrywide swam in.

One last piece of informantion that discredits the “Blame The CRA” meme… The housing crisis was NOT just isolated to the US, it was world-wide. Please tell me how the United States Governments CRA regulations caused the housing markets in Spain, Belgium, the UK, and a host of other countries to experience an even more severe housing bust than we had?

They don’t share the US CRA policies. What they do share, are the same finincial institutions and flawed investment practices that created the financial mess.

That Forbes piece is just short of being propaganda, as some of the figures are wrong, inflated, and totally one sided. But what do you expect from a magazine that caters to the business class.

PS. I am one of that class as I own my own business.

![]() Economics, Journalism, News Critique, Tortured Logic | Sonicfrog June 11, 2014

Economics, Journalism, News Critique, Tortured Logic | Sonicfrog June 11, 2014

RSS feed for comments on this post. TrackBack URI